How to Buy Dividend Stocks: Step-by-Step Guide for Beginners

Dividend stocks have a loyal following for one simple reason: they pay you just for owning them. Whether you're chasing steady income, building long-term wealth, or just want a more resilient portfolio, dividend-paying stocks offer a powerful mix of cash flow and compounding potential. With this approach in mind, let’s turn your portfolio into a passive income machine. Here's a handy step-by-step guide to help you get started.

How to buy dividend stocks

Buying dividend stocks doesn’t need to be complicated. With the right strategy, it can be a smooth and rewarding experience, even for beginners. Here’s how to take your first steps into the world of dividend investing.

1. Open a brokerage account

To invest in dividend stocks, you’ll first need a brokerage account. Most online brokers today offer commission-free trading, fractional shares, and easy-to-use platforms that can help you get started with as little as $100. Popular options include Fidelity, Schwab, Vanguard, and newer platforms like Robinhood or SoFi. What they all have in common is that it’s simple, fast, and free to open most basic brokerage accounts.

2. Decide what type of account to use

You’ll want to consider tax efficiency here because where you hold your dividend stocks can impact how much of your income you actually keep. Some accounts let you grow your dividends tax-free, while others offer more flexibility for accessing cash. Here's a quick breakdown:

- Taxable accounts: Ideal for flexibility, particularly for early retirees or those seeking to tap into dividend income before reaching retirement age. Just know you may owe taxes on what you earn each year.

- Tax-advantaged accounts (like a Roth IRA or traditional IRA): These accounts shield your dividends and capital gains from taxes now or later, making them ideal for compounding returns over time. Roth IRAs are especially powerful investment accounts for investors, as dividend taxes in Roth IRAs can provide significant advantages, including tax-free reinvestments.

3. Research dividend stocks to buy

Not all dividend stocks are created equal. Some offer sustainable, growing income, while others may lure you in with high yields but lack the fundamentals to back them up. Here are some essentials to consider when evaluating potential picks:

- Dividend yield: This tells you how much income a stock pays relative to its share price. Be cautious, as an unusually high yield can be a red flag for underlying business issues.

- Dividend growth rate: A consistent track record of dividend increases is a sign of financial stability and management confidence. Look for companies with multi-year growth streaks.

- Payout ratio: This measures how much of a company’s earnings are paid out as dividends. A moderate payout ratio of less than 60% suggests the dividend is sustainable, leaving room for reinvestment in revenue growth.

- Business fundamentals: Strong cash flow, low debt, and a durable competitive advantage are key traits of companies that can support and grow dividends over time.

If you're just starting out or want a more hands-off approach, consider Dividend Aristocrats, Dividend Kings, or dividend ETFs. These options provide diversified exposure to companies with a proven track record of increasing dividends. We’ve also produced an in-depth guide to the best dividend stocks if you’re looking for specific ideas to research further.

4. Determine how much to invest

Once you've identified the dividend stocks or ETFs you want to buy, it's time to figure out how much to invest. This step is crucial if you have a specific income goal in mind, such as earning $500 per month in dividend income or covering a recurring expense with dividends.

Start by identifying your desired annual dividend income, then work backwards using the average yield of your selected investments. For example, if your goal is $6,000 of dividend income a year and the average dividend yield is 4%, you’d need to invest $150,000 ($6,000 ÷ 0.04).

One general rule of thumb for simplifying the determination of how much to invest is to use the 25x dividend rule. Just multiply your desired annual income by 25 to determine how much you’ll need to invest. This rule assumes a 4% portfolio yield, so you’ll need to multiply by more than 25 if the average portfolio yield is lower.

5. Buy and consider a DRIP

Once you’ve picked your stocks, it’s time to put your plan into action by placing your order through your broker. From there, consider enrolling in a dividend reinvestment plan (DRIP). This powerful tool lets you automatically reinvest your dividend payments into additional shares, no extra effort required. Over time, this reinvestment snowballs into larger payouts, accelerating your portfolio’s compounding potential. It’s a simple, hands-off way to keep your money working for you.

To help you model the impact of reinvesting dividends, try using our dividend calculator. The calculator includes DRIP functionality so you can visualize how reinvested dividends grow your portfolio over time. It’s a great way to set realistic income goals and understand if DRIP investing makes sense for your investing goals.

6. Track your performance

Tracking your dividend portfolio is just as important as building it. Without a clear view of your income and performance, it’s easy to miss signs of trouble or opportunities to optimize.

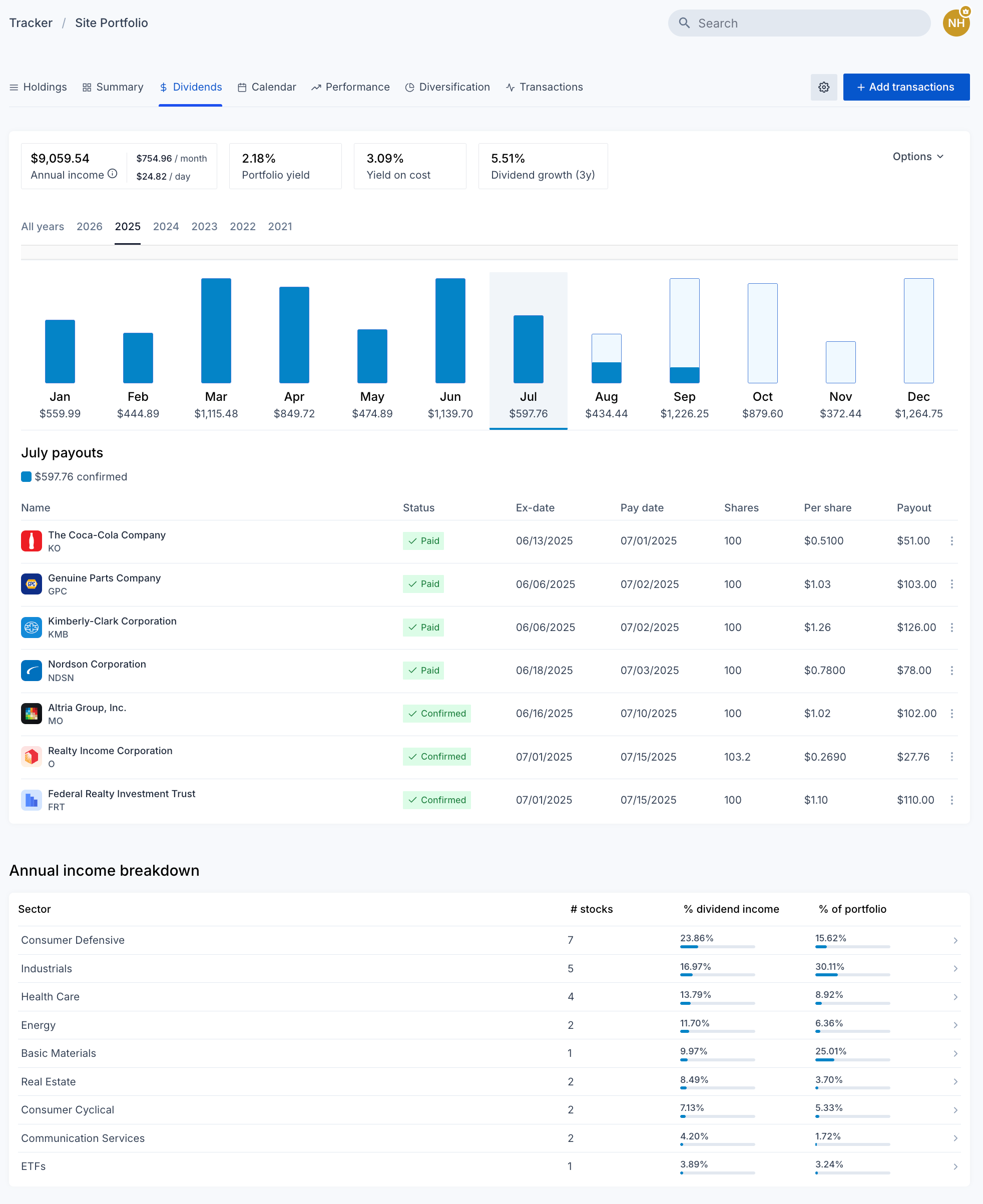

While many brokers offer limited insight into dividend-specific metrics, Dividend Watch’s portfolio tracker is built specifically for dividend investors. It tracks income, yield, diversification, and dividend growth in one place, making it easy to stay on top of your strategy without getting lost in generic dashboards.

The dividend summary view inside Dividend Watch's portfolio tracker provides in-depth dividend analytics that most brokers lack. Source: Dividend Watch

Should you buy dividend stocks?

Dividend stocks are a great fit for investors who want more than just long-term gains. They’re especially appealing for:

- Income seekers: Retirees or early retirees who rely on consistent cash flow to cover expenses without dipping into principal.

- Long-term investors: Those reinvesting dividends can harness the power of compounding, which quietly accelerates growth over time.

- Risk-conscious investors: Dividend-paying companies are often well-established, cash-generating businesses with lower volatility compared to high-growth stocks.

That said, no strategy is perfect. Some high-yield stocks are “yield traps” with unsustainable payouts, and growth stocks may outperform over long horizons. That’s why blending dividend strategies with growth exposure can help create a more resilient, well-rounded portfolio.

Buying dividend ETFs may be a smarter choice

If you're looking for a simpler, lower-maintenance way to invest in dividend-paying companies, dividend ETFs can be a powerful option. They bundle together dozens, or even hundreds, of dividend stocks, offering instant diversification and lower risk from individual stock volatility. Many ETFs also follow strict dividend growth or quality screens, helping you avoid underperformers without needing to research each stock.

Dividend ETFs are especially useful for beginners, time-starved investors, or those managing larger portfolios who want consistent income without having to monitor every company. You still get exposure to dividend income and potential capital appreciation but with less guesswork.

What account should you buy dividend stocks in?

Where you hold dividend stocks can make a big difference in your after-tax returns and in how efficiently your dividends compound over time. Choosing the right account type helps you reduce dividend taxes, maximize reinvestment potential, and align your strategy with your income goals. Here's a breakdown of the key options to consider.

Roth IRA

Ideal for long-term dividend investors. Dividends grow and can be withdrawn tax-free after age 59½ (as long as you meet the 5-year rule). Perfect for DRIP investing and compounding, making it ideal for younger investors focused on compounding.

Traditional IRA or 401(k)

Offers tax-deferred growth. You won’t pay taxes on dividends now, but withdrawals in retirement are taxed as income.

Taxable brokerage account

It offers flexibility, as you can access dividends at any time without incurring early withdrawal penalties, as with IRAs or a 401(k). But you may owe taxes on dividends each year, depending on your income.

Using a mix of these accounts gives you more control over when and how you use your dividend income. For example, taxable accounts let you tap dividends early without penalties, while Roth IRAs grow your income tax-free for the long haul. Traditional IRAs help reduce your taxable income now, even if taxes come later. By strategically spreading your dividend investments across account types, you can manage tax exposure, preserve flexibility, and keep more of your earnings working for you.