How Are Dividends Taxed in 2024–2025? Rates, Rules, and Strategies

Dividends can be a rewarding part of your investment strategy. Free money, right? Not quite. While they do offer income without selling a single share, Uncle Sam still wants his cut.

Understanding how dividend taxes work is key to maximizing the amount you actually keep. In this guide, we’ll walk through how dividends are taxed, what you might owe in 2024 and 2025, strategies to reduce or defer taxes, and more.

How are dividends taxed?

Dividends fall into two main categories for tax purposes: qualified and non-qualified, also referred to as ordinary. The distinction has a significant impact on how much you owe at tax time.

Qualified dividends

Qualified dividends are an investor favorite since they benefit from lower tax rates that match the long-term capital gains rates, which are 0%, 15%, or 20% as of 2025. But there’s a catch: not every dividend is qualified. To receive the qualified dividend tax rate, the dividend must meet all of the following, according to the IRS(1):

- Paid by a US corporation or a qualified foreign corporation.

- Not from a disqualified source (such as REITs or MLPs).

- You must have held the stock for more than 60 days during the 121-day period that begins 60 days before the ex-dividend date.

Let’s run through an example since IRS verbiage is often written for lawyers rather than everyday investors.

Microsoft Corporation (MSFT) had an ex-dividend date of May 15, 2025. You must have held the stock for 61 days between March 16 and July 14. If you buy on March 20 and sell on June 1, you meet the holding requirement, and your dividend is qualified.

Preferred stocks have a longer holding period rule, which is more than 90 days during the 181-day period that begins 90 days before the ex-dividend date.

Non-qualified (ordinary) dividends

If your dividend doesn’t meet the criteria above, it’s considered ordinary income and taxed accordingly. That means up to 37%, depending on your tax bracket. This higher tax rate is the biggest drawback of ordinary dividends.

Common sources of non-qualified dividends include REITs, MLPs, certain foreign companies, and dividends received from stocks you didn’t hold long enough.

In the case of REITs and MLPs, these investments receive certain federal tax advantages when distributing at least 90% of their earnings to shareholders and operate as pass-through entities, which offer high yields. The tradeoff? You’re stuck paying ordinary income tax on those distributions.

Dividend tax rates 2024

Qualified dividend rates are tied to taxable income and filing status. Here is a detailed overview of the 2024 dividend tax rates applicable for taxes due in 2025.

| Tax Rate | Single | Married Filing Jointly | Married Filing Separately | Head of Household |

|---|---|---|---|---|

| 0% | $0-$47,025 | $0-$94,050 | $0-$47,025 | $0-$63,000 |

| 15% | $47,026-$518,900 | $94,051-$583,750 | $47,026-$291,850 | $63,001-$551,350 |

| 20% | $518,901 or more | $583,751 or more | $291,851 or more | $551,351 or more |

Importantly, there is a 0% dividend tax for 2024 in various filing status scenarios, as outlined below.

- Single filing status: $0 to $47,025

- Married filing jointly filing status: $0 to $94,050

- Married filing separately filing status: $0 to $47,025

- Head of household filing status: $0 to $63,000

Dividend tax rates 2025

The brackets inch up slightly in 2025. Here’s how they look:

| Tax Rate | Single | Married Filing Jointly | Married Filing Separately | Head of Household |

|---|---|---|---|---|

| 0% | $0-$48,350 | $0-$96,700 | $0-$48,350 | $0-$64,750 |

| 15% | $48,351-$533,400 | $96,701-$600,050 | $48,350-$300,000 | $64,751-$566,700 |

| 20% | $533,401 or more | $600,051 or more | $300,001 or more | $566,701 or more |

As in 2024, there is a 0% dividend tax for 2025 in the following filing status scenarios.

- Single filing status: $0 to $48,350

- Married filing jointly filing status: $0 to $96,700

- Married filing separately filing status: $0 to $48,350

- Head of household filing status: $0 to $64,750

On the other end of the income spectrum, high-income earners may also owe the 3.8% net investment income tax (NIIT) on top of these rates in 2025.

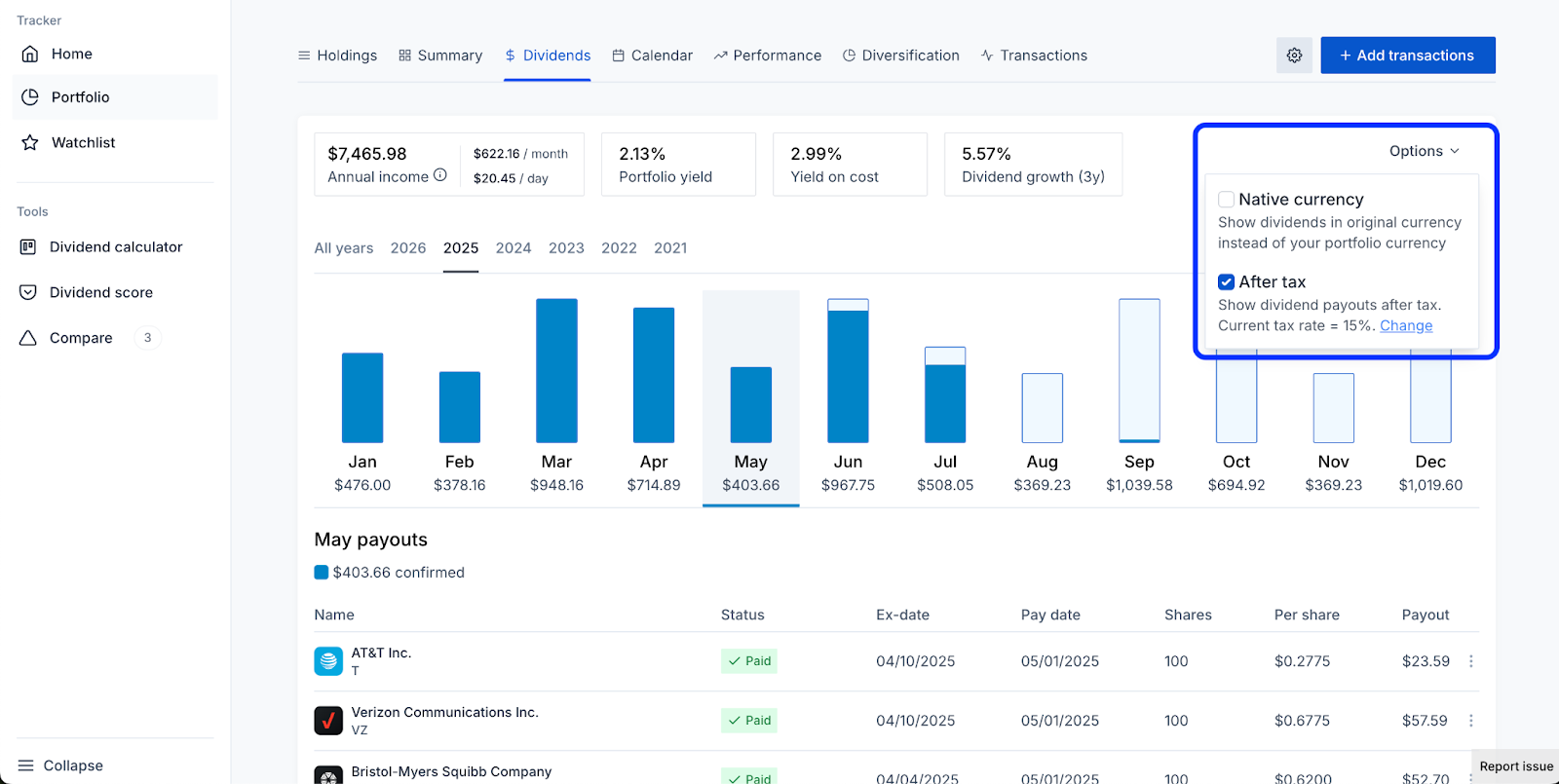

One handy feature we’ve built into Dividend Watch is the ability to set a portfolio-level tax rate, allowing you to gain practical insights into dividend income based on your tax settings.

Set a portfolio-level tax rate inside the Dividend Watch tracker to learn how taxes affect your income and portfolio returns. Source: Dividend Watch

Where are dividend taxes reported?

Come tax time, your broker will send you a Form 1099-DIV. Here’s a quick rundown of where dividends are reported:

- Box 1a for total ordinary dividends

- Box 1b for qualified dividends

If you receive more than $1,500 in ordinary dividends, you also need to file Schedule B with your Form 1040.

Calculating after-tax dividend yield

Many investors overlook assessing their after-tax returns, especially when reviewing dividend yields. It’s an important step, as it provides a realistic picture of what you'll pocket. Thankfully, there’s a quick and simple way to calculate your after-tax dividend yield.

After-Tax Yield = Dividend Yield x (1 - Tax Rate)

Let’s review an example to demonstrate the calculation, assuming a 5% yield and 15% tax rate. The actual return you can expect after taxes is 4.25% (0.05 x 0.85) after the government gets its cut of $750.

Taxes on reinvested dividends

Even if you reinvest dividends through a dividend reinvestment plan (DRIP), they are still taxable in the year received.

The reinvested amount of each dividend becomes part of your cost basis in the stock. This is crucial when calculating capital gains or losses upon sale, so keep accurate records of the date of reinvestment, the number of shares purchased, and the price per share. Most brokers will automatically track the overall cost basis details, simplifying the process for many who invest in dividend stocks.

Without these records, the IRS may assume a $0 cost basis, leading to overstated capital gains.

IRAs and dividend taxes

Using retirement accounts to hold dividend-paying stocks is a popular strategy for deferring or eliminating taxes on dividends. However, tax treatments differ based on the IRA account type.

Like capital gains, dividends earned or reinvested inside a Roth IRA are not taxed, as long as qualified withdrawal rules are met. Our Roth IRA taxes guide goes into more depth on the subject.

Dividends in a Traditional IRA aren’t taxed when earned but are taxed at your ordinary rate when withdrawn, just like any qualified withdrawal.

We’re fans of investing in IRA accounts for these reasons, especially if you qualify to make Roth IRA contributions. You won’t get hit with a tax bill for capital gains and dividends, allowing your investments to compound tax-free.

Taxes on foreign dividends

There’s an extra wrinkle that can add complexity at tax time if you invest in foreign dividend stocks. When you invest in international stocks or funds that hold foreign companies, you may be subject to foreign withholding taxes on the dividends you receive, often deducted automatically before the dividend reaches your account.

Fortunately, you may be able to claim a credit or deduction for those taxes using the Foreign Tax Credit (Form 1116), which helps reduce double taxation.

Not all investors need to file Form 1116. If your total foreign taxes paid are $300 or less ($600 if married filing jointly), you can typically claim the credit directly on your Form 1040.

It’s also worth noting that some foreign dividends may not qualify for the lower qualified dividend tax rates, depending on the issuing country and how long you held the investment.

Dividend taxes for other investment types

The tax treatment for other security types can vary depending on the investment vehicle.

ETFs

ETFs pass along dividends from the stocks they hold. If those dividends are qualified at the fund level and you meet the holding period requirement for the ETF, they may be taxed at the qualified rate, just like stocks.

REITs

Dividend distributions from REITs are typically non-qualified and taxed at ordinary income rates, as these corporate structures already receive tax advantages as pass-through entities.

Preferred stocks

Preferred dividends are typically qualified. However, the holding requirement is stricter, with a 90-day holding period within a 181-day period that begins 90 days before the ex-dividend date.

FAQ

How can you avoid dividend taxes?

To avoid taxes on dividends, consider holding dividend-paying stocks in a Roth IRA, where qualified withdrawals are not taxed. Additionally, you can reduce your taxable income to fall within the 0% qualified dividend tax bracket, effectively eliminating federal taxes on qualified dividends.

Are reinvested dividends taxable?

Yes. Even if you reinvest dividends in a taxable brokerage account, they are still reported as income and taxed in the year you received them. The reinvested amount increases your cost basis, potentially reducing future capital gains. Reinvested dividends are not taxed in a Roth IRA, letting your investments grow tax-free in this type of tax-advantaged account.

Sources

1. IRS Publication 550. IRS, https://www.irs.gov/forms-pubs/about-publication-550.