Dividend Reinvestment Plans (DRIPs): A Guide to Growing Income Automatically

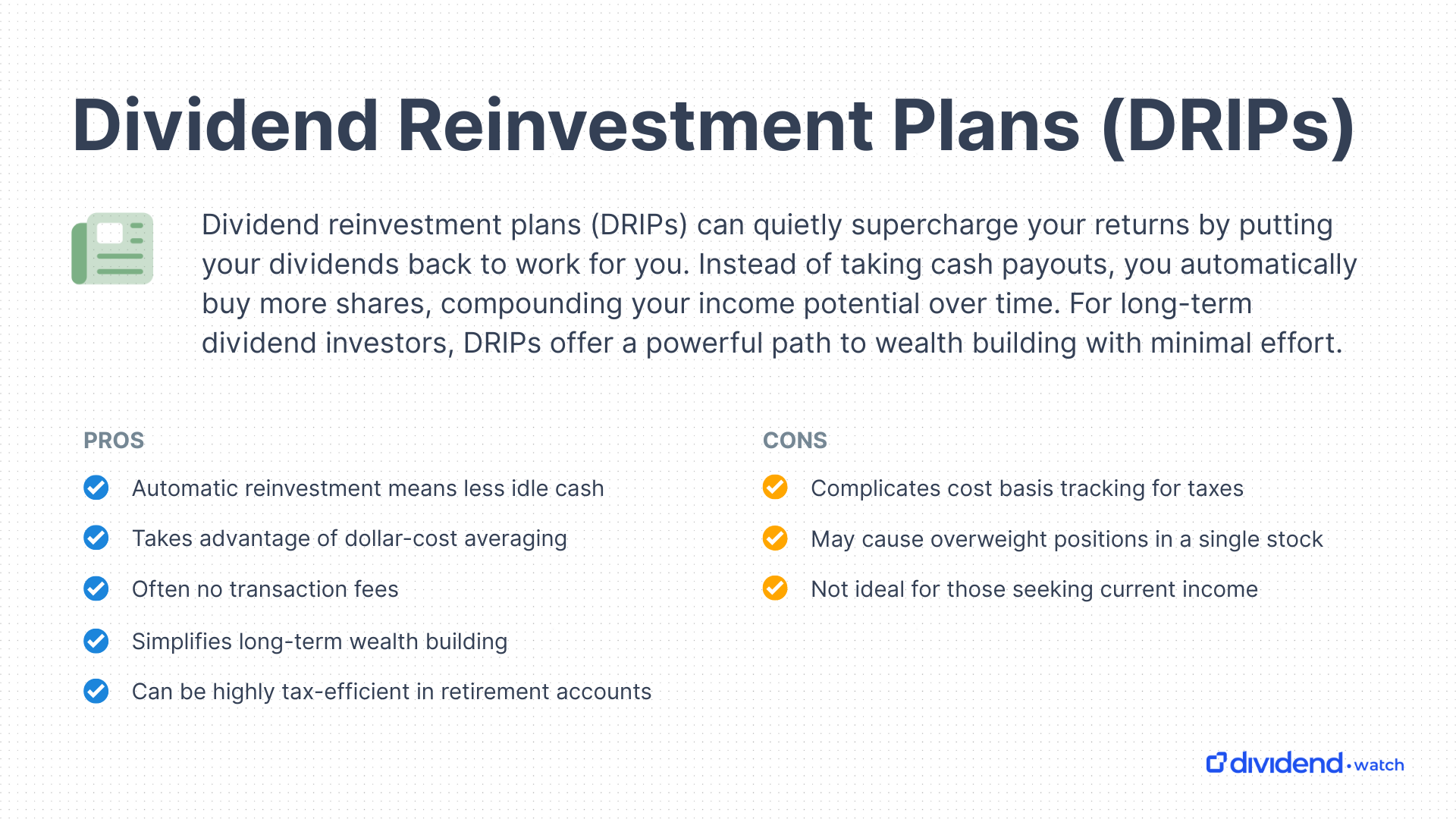

Dividend reinvestment plans (DRIPs) can quietly supercharge your returns by putting your dividends back to work for you. Instead of taking cash payouts, you automatically buy more shares, compounding your income potential over time. For long-term dividend investors, DRIPs offer a powerful path to wealth building with minimal effort.

With this in mind, let’s break down how they work, when to use them, and how Dividend Watch supports DRIP-focused investing.

What Is A Stock Dividend Reinvestment Plan?

A DRIP is a program that allows investors to automatically reinvest their cash dividends into additional shares of the same stock or ETF. Instead of receiving a cash payout, you receive more shares, sometimes even fractional shares, of the company.

There are two common types of DRIP plans:

- Brokerage DRIPs: Most online brokers offer DRIP functionality that automatically reinvests dividends in the same stock.

- Company-sponsored DRIPs: Offered directly by some companies, these plans may include perks such as discounted share prices or no fees.

While DRIPs are simple in concept, their long-term benefits lie in compounding.

How DRIPs Turbocharge Compounding

When you reinvest dividends, those new shares generate dividends of their own. Over time, this cycle builds momentum and magnifies your total returns as both your rising share counts and dividends buy more shares at each payout event.

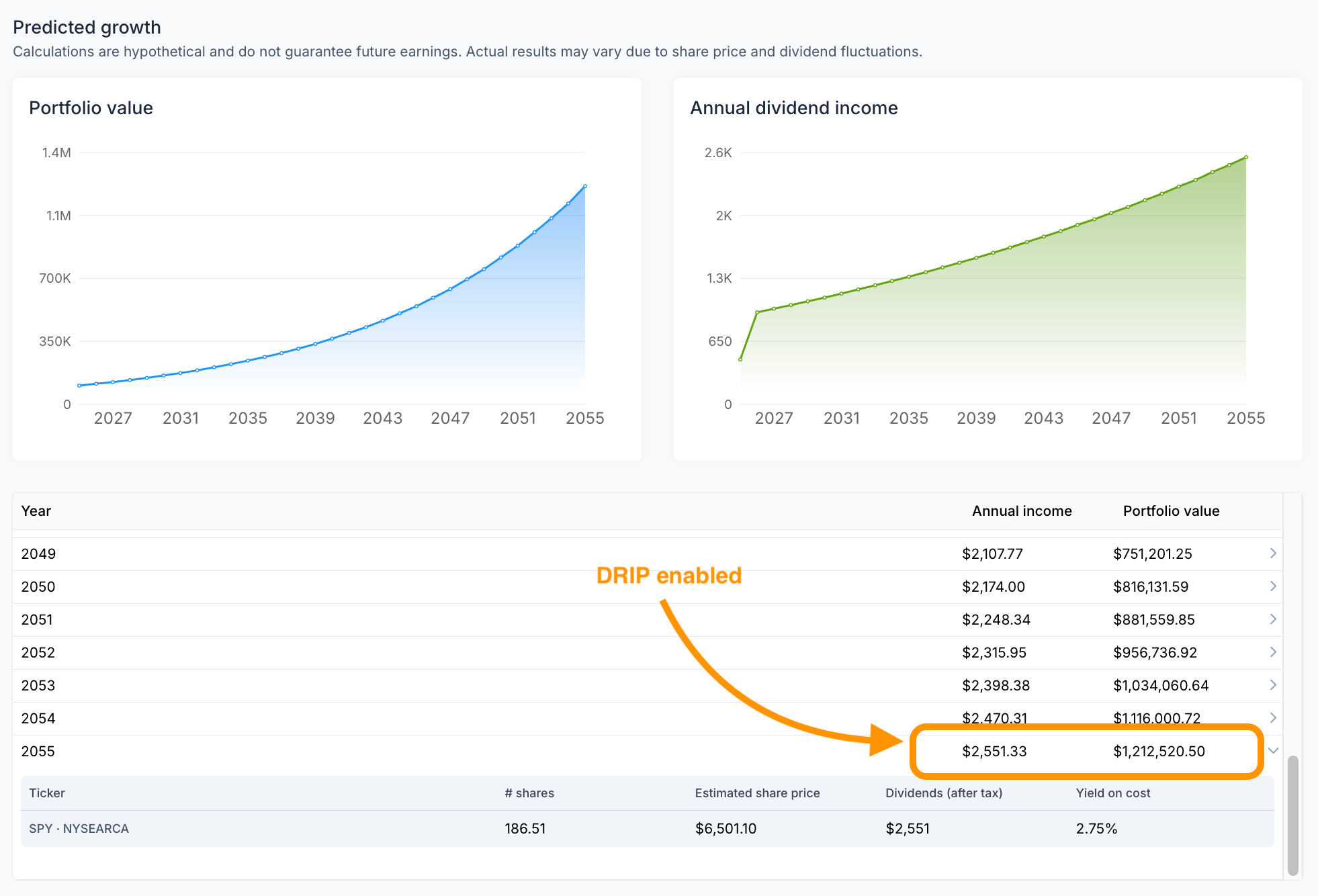

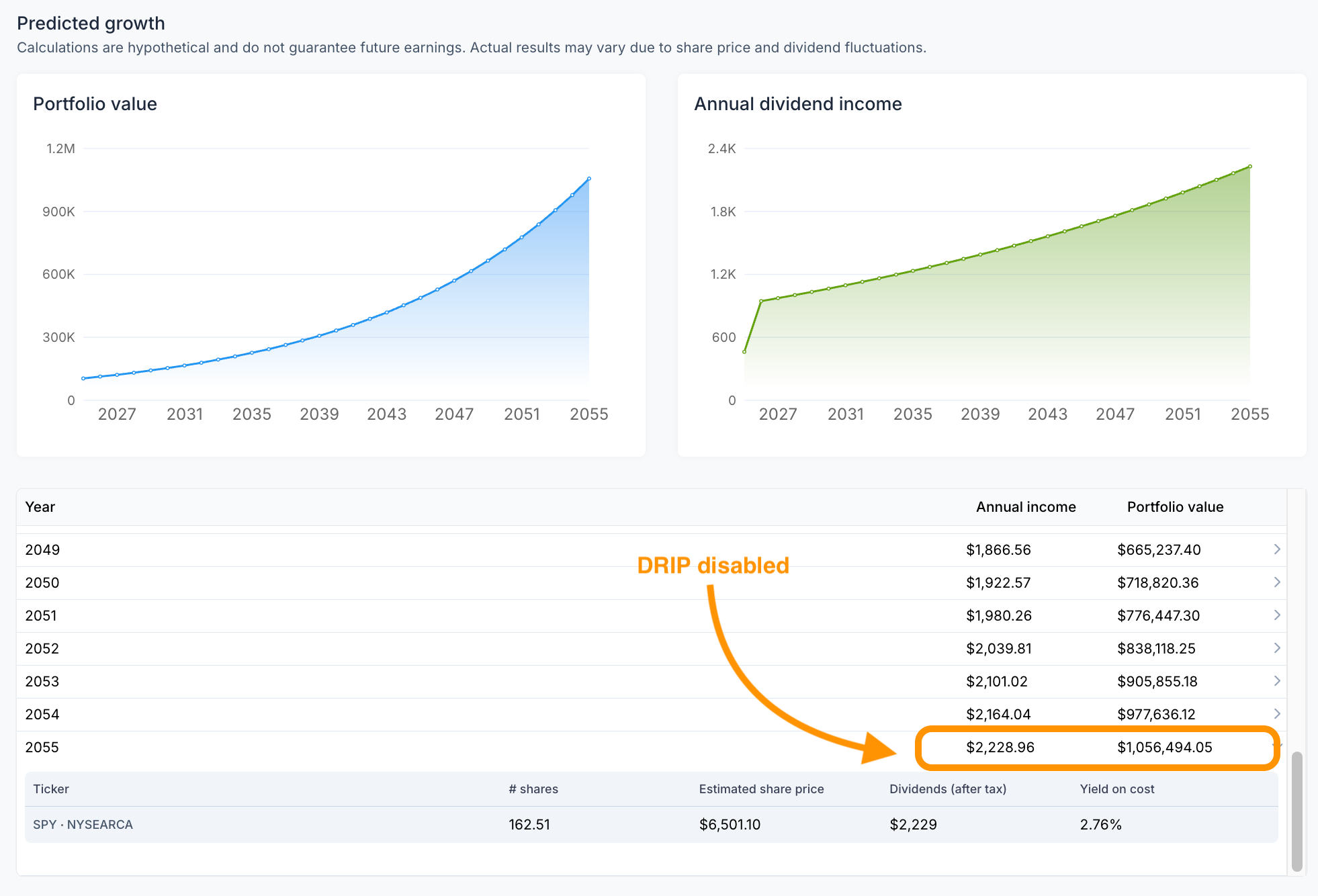

Let’s demonstrate the wealth-compounding benefits with an example using our DRIP dividend calculator. Say you invest $100,000 in the SPDR S&P 500 ETF (SPY) for 30 years, at an 8% annualized growth rate, and a 3% dividend growth rate.

With DRIP enabled, you’d have an ending portfolio value $1.212 million and 186.51 SPY shares. On the other hand, you’d have $1.056 million and 162.51 SPY shares with DRIP disabled. By simply enabling dividend reinvestment, you’d automatically be $156,000 richer.

Estimated portfolio value with DRIP enabled: Source: Dividend Watch

Estimated portfolio value with DRIP disabled: Source: Dividend Watch

The ideal DRIP stocks are often dividend growth stocks that have established track records of increased payouts. This process of double-compounding dividend and share growth can generate impressive results.

However, DRIPs aren’t the best option for every investor. If you’re retired or rebalancing often, consider pausing DRIPs in favor of cash payouts to cover expenses or rebalance your portfolio.

Tax Considerations

In taxable accounts, reinvested dividends are still considered taxable income in the year received, even though you don’t see the cash.

Each reinvested dividend creates a new tax lot, which can make cost basis tracking tricky.

This complexity is one reason why we suggest using DRIPs in tax-advantaged accounts, especially Roth IRAs. Dividends can grow tax-free by taking advantage of select Roth IRA dividend tax rules that keep Uncle Sam from taking his cut.

How to Set Up a DRIP

Setting up a DRIP in your brokerage account is straightforward with the check of a box. Most online brokers offer the option to automatically reinvest dividends when you purchase a stock. You can typically select this option during the initial buy transaction or enable it later in your account settings. Once activated, any dividends paid will be reinvested into additional shares without needing to lift a finger.

Even if your broker doesn’t show DRIP results clearly (trust us, we’ve tried!), tools like Dividend Watch help you track the effects of reinvestment.

When NOT to Use a DRIP

There are situations where opting for cash dividends is a smarter choice than reinvesting them. Here are a few of those scenarios:

- You rely on dividends for regular income

- You want to rebalance into better-valued assets

- You want to build a cash position

Using Dividend Watch for DRIP Investing

Dividend Watch was built with dividend-focused investors in mind. So, of course, our dividend portfolio tracker includes DRIP functionality. Most brokerages focus on account balances. Dividend Watch shows you the compounding power of dividend reinvestment. Here’s a brief overview of the DRIP features integrated into Dividend Watch:

Individual Stock Drip Functionality

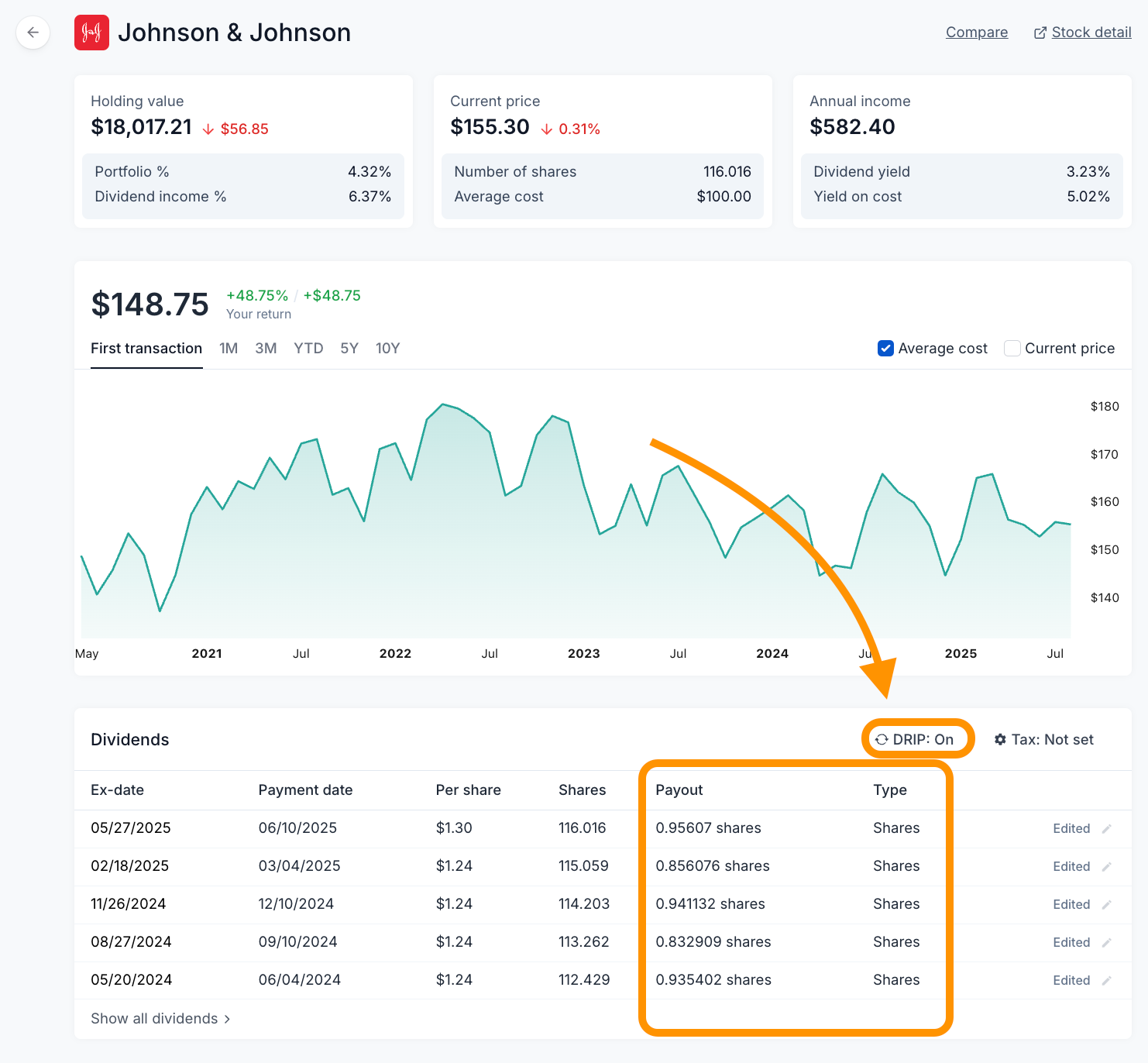

You can enable DRIP for individual stocks tracked in your portfolio, automatically showing how your dividend income, share count, and percentage returns grow over time.

Enable DRIP functionality for individual stock holdings to get detailed income and return insights: Source: Dividend Watch

Advanced DRIP Strategies

Once you’ve mastered the basics of dividend reinvestment, you can start applying more advanced tactics to amplify results and stay aligned with your broader goals, including the following tactics:

- Target dividend growth stocks: These not only increase your share count through reinvestment, but also raise the dividend per share over time, compounding income growth even faster as the cycle repeats.

- Use DRIP in retirement accounts: Take full advantage of tax-free compounding in Roth IRAs and tax-deferred growth in traditional IRAs.

- Rebalance with intent: Review your portfolio periodically to prevent overconcentration in any one stock or sector due to continuous reinvestment.

- Use yield on cost: Track how your income grows relative to your original investment, an effective way to measure long-term reinvestment success.

One proof-in-the-pudding advanced tactic investors utilize is to turn DRIPs off when a stock becomes overvalued and manually reinvest into more attractive opportunities. This is the precise approach Warren Buffett employs, preferring to pocket the income that Berkshire Hathaway’s dividend stocks dish out in favor of deploying that cash into the highest-value opportunity at any given moment.

But consider that this advanced approach only makes sense for seasoned investors with successful stock-picking track records.

FAQ

Do all stocks support DRIPs?

No, but most dividend-paying stocks and ETFs at major brokerages can be set up for reinvestment.

Are DRIPs better than cash dividends?

It depends on your goals. DRIPs are better for growth investors in the accumulation phase; cash is better for income investors, such as retirees, who cover their expenses with dividends.

Can you reinvest dividends in a Roth IRA?

Yes, and it's one of the best ways to grow tax-free retirement income.

How do you track reinvested dividends?

Most brokers offer limited DRIP insights, including information on how reinvesting affects portfolio values and returns. Use Dividend Watch to automatically access these insights and understand how DRIP affects returns and portfolio values.

What happens to partial shares when reinvesting dividends?

Most brokers will credit you with fractional shares when the dividend isn’t enough to buy a full share. These fractional shares behave just like full shares. They earn dividends and continue to compound your investment over time.